by Calculated Threat on 6/09/2025 01:49:00 PM

Early in February, I expressed my “growing concern” in regards to the destructive financial impression of “govt / fiscal coverage errors”, nevertheless, I concluded that publish by noting that I used to be not at the moment on recession watch.

Final month Warren Buffett mentioned:

“We ought to be trying to commerce with the remainder of the world, and we should always do what we do finest, and they need to do what they do finest … Commerce shouldn’t be a weapon.”

Within the quick time period, it’s largely commerce coverage that may negatively impression the financial system. Nonetheless, there different elements of coverage that bear watching.

Right here is a number of the information I am watching.

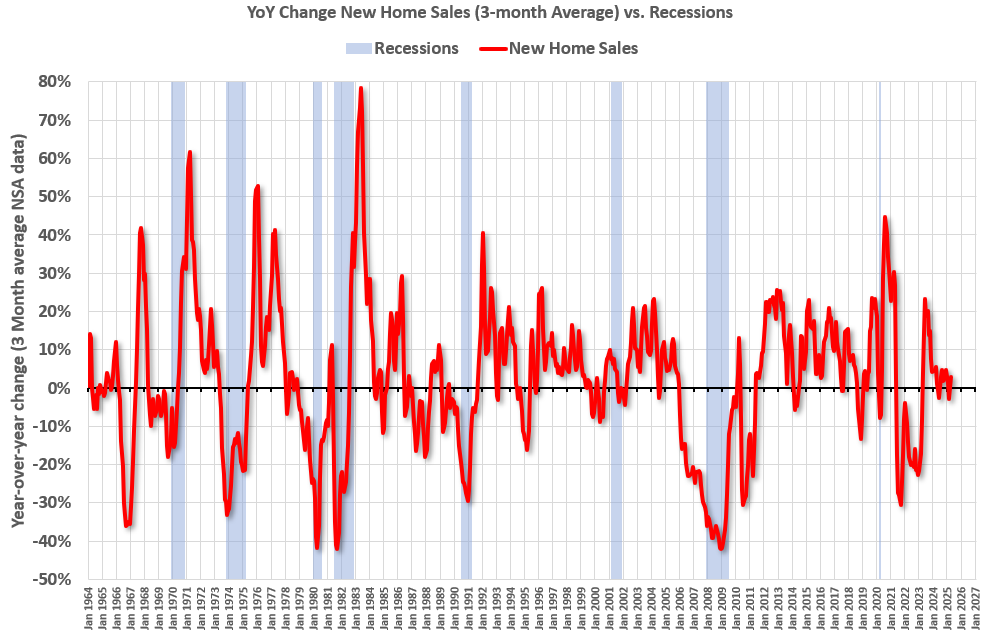

Housing: Housing is the idea of certainly one of my favourite fashions for enterprise cycle forecasting.

This graph exhibits the YoY change in New House Gross sales from the Census Bureau. At present new dwelling gross sales (based mostly on 3-month common of NSA information) are up 3% year-over-year.

This graph exhibits the YoY change in New House Gross sales from the Census Bureau. At present new dwelling gross sales (based mostly on 3-month common of NSA information) are up 3% year-over-year.Normally when the YoY change in New House Gross sales falls about 20%, a recession will observe. An exception for this information sequence was the mid ’60s when the Vietnam buildup stored the financial system out of recession. One other exception was in late 2021 – we noticed a major YoY decline in new dwelling gross sales associated to the pandemic and the surge in new dwelling gross sales within the second half of 2020. I ignored that downturn as a pandemic distortion. Additionally word that the sharp decline in 2010 was associated to the housing tax credit score coverage in 2009 – and was only a continuation of the housing bust.

The YoY change in new dwelling gross sales in late 2022 and early 2023 recommended a potential recession. However as I famous earlier, I used to be in a position to look previous the pandemic distortion and was in a position to predict a pickup in new dwelling gross sales because of the low stage of current dwelling stock and since homebuilders might provide mortgage incentives that might considerably offset the sharp enhance in mortgage charges.

There aren’t any particular circumstances now, and if this measure falls to off 20% a recession appears possible.

Yield Curve: The yield curve is a generally used main indicator. I dismissed it when the yield curve inverted in 2019 and once more in 2022. Each occasions dismissing the yield curve was appropriate (the recession in 2020 was clearly because of the pandemic, so we’ll by no means know if the yield curve did not predict a recession in 2019).

Here’s a graph of 10-Yr Treasury Fixed Maturity Minus 2-Yr Treasury Fixed Maturity from FRED since 1976.

Heavy Truck (and Automobile Gross sales): One other indicator I like to make use of is heavy truck gross sales. This graph exhibits heavy truck gross sales since 1967 utilizing information from the BEA. The dashed line is the Might 2025 seasonally adjusted annual gross sales fee (SAAR). Word: “Heavy vehicles – vehicles greater than 14,000 kilos gross car weight.”

Heavy truck gross sales have been at 446 thousand SAAR in Might, down from 457 thousand in April, and down 7.9% from 484 thousand SAAR in Might 2024.

Normally, heavy truck gross sales decline sharply previous to a recession and gross sales have been OK in Might.

And lightweight car gross sales have been okay in Might after surging in March and April as patrons rushed to beat the tariffs.

And lightweight car gross sales have been okay in Might after surging in March and April as patrons rushed to beat the tariffs.

Gentle car gross sales in Might (15.65 million SAAR) have been down 9.4% from April, and down 1.1% from Might 2024.

Unemployment: Two different concurrent indicators are the unemployment fee (utilizing the “Sahm Rule”) and weekly unemployment claims.

Here’s a graph of the Sahm rule from FRED since 1959.

Here’s a graph of the Sahm rule from FRED since 1959.

The Sahm Rule was at 0.27 in Might.

And weekly unemployment claims at all times rise sharply originally of a recession (different occasions – like hurricane Katrina – may cause a short lived spike in weekly claims).

And weekly unemployment claims at all times rise sharply originally of a recession (different occasions – like hurricane Katrina – may cause a short lived spike in weekly claims).

As I famous earlier, I am undecided estimate the financial injury brought on by these tariffs. They usually would possibly simply go away (nobody is aware of). There are additionally boycotts of U.S. items and fewer worldwide tourism based mostly on each the tariffs and the inflammatory rhetoric of the present administration.

by Calculated Threat on 6/09/2025 01:49:00 PM

Early in February, I expressed my “growing concern” in regards to the destructive financial impression of “govt / fiscal coverage errors”, nevertheless, I concluded that publish by noting that I used to be not at the moment on recession watch.

Final month Warren Buffett mentioned:

“We ought to be trying to commerce with the remainder of the world, and we should always do what we do finest, and they need to do what they do finest … Commerce shouldn’t be a weapon.”

Within the quick time period, it’s largely commerce coverage that may negatively impression the financial system. Nonetheless, there different elements of coverage that bear watching.

Right here is a number of the information I am watching.

Housing: Housing is the idea of certainly one of my favourite fashions for enterprise cycle forecasting.

This graph exhibits the YoY change in New House Gross sales from the Census Bureau. At present new dwelling gross sales (based mostly on 3-month common of NSA information) are up 3% year-over-year.Normally when the YoY change in New House Gross sales falls about 20%, a recession will observe. An exception for this information sequence was the mid ’60s when the Vietnam buildup stored the financial system out of recession. One other exception was in late 2021 – we noticed a major YoY decline in new dwelling gross sales associated to the pandemic and the surge in new dwelling gross sales within the second half of 2020. I ignored that downturn as a pandemic distortion. Additionally word that the sharp decline in 2010 was associated to the housing tax credit score coverage in 2009 – and was only a continuation of the housing bust.

The YoY change in new dwelling gross sales in late 2022 and early 2023 recommended a potential recession. However as I famous earlier, I used to be in a position to look previous the pandemic distortion and was in a position to predict a pickup in new dwelling gross sales because of the low stage of current dwelling stock and since homebuilders might provide mortgage incentives that might considerably offset the sharp enhance in mortgage charges.

There aren’t any particular circumstances now, and if this measure falls to off 20% a recession appears possible.

Yield Curve: The yield curve is a generally used main indicator. I dismissed it when the yield curve inverted in 2019 and once more in 2022. Each occasions dismissing the yield curve was appropriate (the recession in 2020 was clearly because of the pandemic, so we’ll by no means know if the yield curve did not predict a recession in 2019).

Here’s a graph of 10-Yr Treasury Fixed Maturity Minus 2-Yr Treasury Fixed Maturity from FRED since 1976.

Heavy Truck (and Automobile Gross sales): One other indicator I like to make use of is heavy truck gross sales. This graph exhibits heavy truck gross sales since 1967 utilizing information from the BEA. The dashed line is the Might 2025 seasonally adjusted annual gross sales fee (SAAR). Word: “Heavy vehicles – vehicles greater than 14,000 kilos gross car weight.”

Heavy truck gross sales have been at 446 thousand SAAR in Might, down from 457 thousand in April, and down 7.9% from 484 thousand SAAR in Might 2024.

Normally, heavy truck gross sales decline sharply previous to a recession and gross sales have been OK in Might.

And lightweight car gross sales have been okay in Might after surging in March and April as patrons rushed to beat the tariffs.

Gentle car gross sales in Might (15.65 million SAAR) have been down 9.4% from April, and down 1.1% from Might 2024.

Unemployment: Two different concurrent indicators are the unemployment fee (utilizing the “Sahm Rule”) and weekly unemployment claims.

Here’s a graph of the Sahm rule from FRED since 1959.

The Sahm Rule was at 0.27 in Might.

And weekly unemployment claims at all times rise sharply originally of a recession (different occasions – like hurricane Katrina – may cause a short lived spike in weekly claims).

As I famous earlier, I am undecided estimate the financial injury brought on by these tariffs. They usually would possibly simply go away (nobody is aware of). There are additionally boycotts of U.S. items and fewer worldwide tourism based mostly on each the tariffs and the inflammatory rhetoric of the present administration.

by Calculated Threat on 6/09/2025 01:49:00 PM

Early in February, I expressed my “growing concern” in regards to the destructive financial impression of “govt / fiscal coverage errors”, nevertheless, I concluded that publish by noting that I used to be not at the moment on recession watch.

Final month Warren Buffett mentioned:

“We ought to be trying to commerce with the remainder of the world, and we should always do what we do finest, and they need to do what they do finest … Commerce shouldn’t be a weapon.”

Within the quick time period, it’s largely commerce coverage that may negatively impression the financial system. Nonetheless, there different elements of coverage that bear watching.

Right here is a number of the information I am watching.

Housing: Housing is the idea of certainly one of my favourite fashions for enterprise cycle forecasting.

This graph exhibits the YoY change in New House Gross sales from the Census Bureau. At present new dwelling gross sales (based mostly on 3-month common of NSA information) are up 3% year-over-year.Normally when the YoY change in New House Gross sales falls about 20%, a recession will observe. An exception for this information sequence was the mid ’60s when the Vietnam buildup stored the financial system out of recession. One other exception was in late 2021 – we noticed a major YoY decline in new dwelling gross sales associated to the pandemic and the surge in new dwelling gross sales within the second half of 2020. I ignored that downturn as a pandemic distortion. Additionally word that the sharp decline in 2010 was associated to the housing tax credit score coverage in 2009 – and was only a continuation of the housing bust.

The YoY change in new dwelling gross sales in late 2022 and early 2023 recommended a potential recession. However as I famous earlier, I used to be in a position to look previous the pandemic distortion and was in a position to predict a pickup in new dwelling gross sales because of the low stage of current dwelling stock and since homebuilders might provide mortgage incentives that might considerably offset the sharp enhance in mortgage charges.

There aren’t any particular circumstances now, and if this measure falls to off 20% a recession appears possible.

Yield Curve: The yield curve is a generally used main indicator. I dismissed it when the yield curve inverted in 2019 and once more in 2022. Each occasions dismissing the yield curve was appropriate (the recession in 2020 was clearly because of the pandemic, so we’ll by no means know if the yield curve did not predict a recession in 2019).

Here’s a graph of 10-Yr Treasury Fixed Maturity Minus 2-Yr Treasury Fixed Maturity from FRED since 1976.

Heavy Truck (and Automobile Gross sales): One other indicator I like to make use of is heavy truck gross sales. This graph exhibits heavy truck gross sales since 1967 utilizing information from the BEA. The dashed line is the Might 2025 seasonally adjusted annual gross sales fee (SAAR). Word: “Heavy vehicles – vehicles greater than 14,000 kilos gross car weight.”

Heavy truck gross sales have been at 446 thousand SAAR in Might, down from 457 thousand in April, and down 7.9% from 484 thousand SAAR in Might 2024.

Normally, heavy truck gross sales decline sharply previous to a recession and gross sales have been OK in Might.

And lightweight car gross sales have been okay in Might after surging in March and April as patrons rushed to beat the tariffs.

Gentle car gross sales in Might (15.65 million SAAR) have been down 9.4% from April, and down 1.1% from Might 2024.

Unemployment: Two different concurrent indicators are the unemployment fee (utilizing the “Sahm Rule”) and weekly unemployment claims.

Here’s a graph of the Sahm rule from FRED since 1959.

The Sahm Rule was at 0.27 in Might.

And weekly unemployment claims at all times rise sharply originally of a recession (different occasions – like hurricane Katrina – may cause a short lived spike in weekly claims).

As I famous earlier, I am undecided estimate the financial injury brought on by these tariffs. They usually would possibly simply go away (nobody is aware of). There are additionally boycotts of U.S. items and fewer worldwide tourism based mostly on each the tariffs and the inflammatory rhetoric of the present administration.

by Calculated Threat on 6/09/2025 01:49:00 PM

Early in February, I expressed my “growing concern” in regards to the destructive financial impression of “govt / fiscal coverage errors”, nevertheless, I concluded that publish by noting that I used to be not at the moment on recession watch.

Final month Warren Buffett mentioned:

“We ought to be trying to commerce with the remainder of the world, and we should always do what we do finest, and they need to do what they do finest … Commerce shouldn’t be a weapon.”

Within the quick time period, it’s largely commerce coverage that may negatively impression the financial system. Nonetheless, there different elements of coverage that bear watching.

Right here is a number of the information I am watching.

Housing: Housing is the idea of certainly one of my favourite fashions for enterprise cycle forecasting.

This graph exhibits the YoY change in New House Gross sales from the Census Bureau. At present new dwelling gross sales (based mostly on 3-month common of NSA information) are up 3% year-over-year.Normally when the YoY change in New House Gross sales falls about 20%, a recession will observe. An exception for this information sequence was the mid ’60s when the Vietnam buildup stored the financial system out of recession. One other exception was in late 2021 – we noticed a major YoY decline in new dwelling gross sales associated to the pandemic and the surge in new dwelling gross sales within the second half of 2020. I ignored that downturn as a pandemic distortion. Additionally word that the sharp decline in 2010 was associated to the housing tax credit score coverage in 2009 – and was only a continuation of the housing bust.

The YoY change in new dwelling gross sales in late 2022 and early 2023 recommended a potential recession. However as I famous earlier, I used to be in a position to look previous the pandemic distortion and was in a position to predict a pickup in new dwelling gross sales because of the low stage of current dwelling stock and since homebuilders might provide mortgage incentives that might considerably offset the sharp enhance in mortgage charges.

There aren’t any particular circumstances now, and if this measure falls to off 20% a recession appears possible.

Yield Curve: The yield curve is a generally used main indicator. I dismissed it when the yield curve inverted in 2019 and once more in 2022. Each occasions dismissing the yield curve was appropriate (the recession in 2020 was clearly because of the pandemic, so we’ll by no means know if the yield curve did not predict a recession in 2019).

Here’s a graph of 10-Yr Treasury Fixed Maturity Minus 2-Yr Treasury Fixed Maturity from FRED since 1976.

Heavy Truck (and Automobile Gross sales): One other indicator I like to make use of is heavy truck gross sales. This graph exhibits heavy truck gross sales since 1967 utilizing information from the BEA. The dashed line is the Might 2025 seasonally adjusted annual gross sales fee (SAAR). Word: “Heavy vehicles – vehicles greater than 14,000 kilos gross car weight.”

Heavy truck gross sales have been at 446 thousand SAAR in Might, down from 457 thousand in April, and down 7.9% from 484 thousand SAAR in Might 2024.

Normally, heavy truck gross sales decline sharply previous to a recession and gross sales have been OK in Might.

And lightweight car gross sales have been okay in Might after surging in March and April as patrons rushed to beat the tariffs.

Gentle car gross sales in Might (15.65 million SAAR) have been down 9.4% from April, and down 1.1% from Might 2024.

Unemployment: Two different concurrent indicators are the unemployment fee (utilizing the “Sahm Rule”) and weekly unemployment claims.

Here’s a graph of the Sahm rule from FRED since 1959.

The Sahm Rule was at 0.27 in Might.

And weekly unemployment claims at all times rise sharply originally of a recession (different occasions – like hurricane Katrina – may cause a short lived spike in weekly claims).

As I famous earlier, I am undecided estimate the financial injury brought on by these tariffs. They usually would possibly simply go away (nobody is aware of). There are additionally boycotts of U.S. items and fewer worldwide tourism based mostly on each the tariffs and the inflammatory rhetoric of the present administration.

{kind=link}