A few months in the past now I wrote a submit in regards to the new set of low cost charges authorities businesses are supposed to make use of in endeavor cost-benefit evaluation, whether or not for brand new spending initiatives or for regulatory initiatives. The brand new, radically altered, framework had come into impact from 1 October final 12 months, however with no publicity (besides to the general public sector businesses required to make use of them). The brand new framework, with a lot decrease low cost charges for many core public sector issues, wasn’t precisely hidden nevertheless it wasn’t marketed both.

My earlier submit (most likely greatest learn along with this one) was primarily based largely round a public seminar Treasury did lastly host in February, the advert for which had belatedly alerted me to this substantial change of coverage strategy (and despatched me off to numerous background paperwork on The Treasury web site).

As a fast reminder, low cost charges matter (usually loads), as they convert future prices and advantages again into equal in the present day’s {dollars} (current values). The low cost price used makes an enormous distinction: for a profit in 30 years time discounting at 2 per cent each year reduces the worth by nearly half, whereas transformed at 8 per cent the current worth of that profit is decreased by nearly 90 per cent.

Till final October, initiatives and initiatives had been to be evaluated at a 5 per cent actual low cost price – slightly decrease than the charges traditionally utilized in New Zealand, however not inconsistent with the document low actual rates of interest skilled across the flip of the last decade (recall that the low cost charges didn’t try to mimic a bond price, however took account of the price of each debt and fairness).

The brand new framework, summarised in a single desk, is

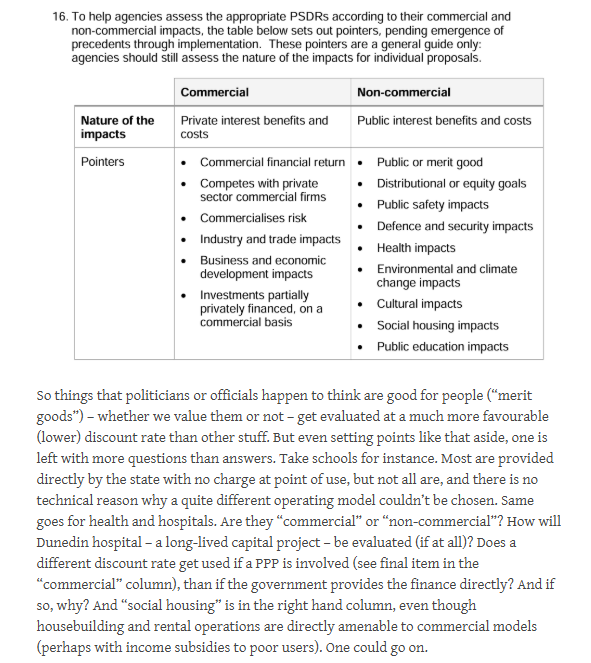

and in case there was any ambiguity about the place the main focus now lay, not solely was the non-commercial proposals line listed first however the round itself made it clear that the non-commercial price(s) had been more likely to be the norm for many public service and Crown entity proposals.

Within the earlier submit I outlined a bunch of considerations about this new strategy, each across the substance and what it would imply for future spending (and, for that matter, regulatory) pressures, and round what appeared to have been fairly a rare course of, with no public session in any respect. Treasury officers on the seminar had, nevertheless, assured me that it had all been authorised by the Minister of Finance, which frankly appeared a bit odd given the (then) new authorities’s rhetorical give attention to rigorous analysis of spending proposals and so on.

Anyway, I went dwelling and lodged an Official Data Act request with The Treasury. They dealt with it pretty expeditiously nevertheless it took me some time to get spherical to working my manner by means of the 100+ pages they supplied. This was the discharge they made to me

Treasury OIA re Public Sector Low cost Charges March 2025

and this was their recommendation to the Minister of Finance, already launched however buried very deep in an enormous normal launch on a spread of matters. I’ve saved it right here as a separate doc.

Treasury Report: Updates to Public Sector Low cost Charges 30 July 2024

Not one of the launched materials allayed any of my considerations. In reality, these considerations at the moment are amplified, and added to them is a priority in regards to the actually poor high quality, and loaded nature, of the slim recommendation supplied to the Minister of Finance on what may be actually fairly a technical problem however with a lot wider potential political economic system implications. There was an finish to be achieved – officers had been eager on decrease low cost charges – and by no means thoughts a cautious. balanced, and complete perspective. It was maybe summed up within the remark from one principal adviser who famous “I get a bit misplaced on the technical forwards and backwards on SOC vs SRTP” however “I assist shifting to 2%”.

Considerably amazingly, though all of the paperwork speak about how a change of this type actually ought to have ministerial approval – that is even documented within the minutes of The Treasury’s Government Management Group assembly of 12 March 2024 – ultimately all they did was ask the Minister to notice the change they (officers) had been making. All of the Minister was requested to comply with was course of stuff across the begin date and future critiques. I’m stunned that there appears to have been nobody in her workplace – her non-Treasury advisers, who partly are supposed to guard busy and non-technical ministers from officers with an agenda – who seems to have appreciated the importance of what was happening or thus to have triggered a request for extra and higher evaluation/recommendation. And even, it seems, to have raised questions on what was behind the remark within the Session part of the paper that “To handle dangers of elevating exterior expectations and a danger of extended debate, we’ve not consulted publicly”. Had been there maybe various views then that the Minister ought to have been made conscious of? (The one individuals consulted had been different public sector chief economists – whose businesses will usually be eager on getting venture analysis thresholds lowered – and some handpicked consultants.)

What turned extra obvious within the papers was that this complete venture had obtained going below the earlier authorities (Labour, however with Greens ministers) when the Parliamentary Commissioner for the Surroundings had instructed in 2021 that public low cost charges needs to be reviewed with a view to adopting a mannequin that might low cost future advantages (relative to upfront prices) much less closely. Treasury had undertaken in 2022 to the (then Labour majority) choose committee that they’d do a overview. Issues appeared to get their very own momentum from there, and nothing about both a change in fiscal circumstances – again in 2021/22 even Treasury was eager on spraying public cash round – nor a change in authorities appears to have prompted a pause. Had the brand new Minister of Finance, or her workplace, been extra alert to the implications, maybe they’d have referred to as a halt to the work programme (however on this event I’m reluctant to place a lot blame on the Minister, as she seems to have been so badly suggested by The Treasury).

The one recommendation the Minister of Finance seems to have been supplied with is the brief paper linked to above. It has simply over two pages of substance (the remaining is course of, plus a 4 web page technical appendix – which I’d think about that, for a noting suggestion solely, a busy – and non-technical – minister wouldn’t usually learn).

It’s placing what the Minister isn’t advised:

- there is no such thing as a point out within the paper that the sensible implication of the brand new strategy Treasury was planning to take was that the majority public sector initiatives and proposals can be evaluated main at a 2 per cent actual low cost price slightly than the (customary) 5 per cent price beforehand. They point out that the SOC-based price is being elevated, in step with the rise in bond charges, however by no means that this low cost price will not be used a lot.

- there is no such thing as a try within the paper to the Minister to clarify, or justify, the brand new strategy below which low cost charges for years past 12 months 30 can be evaluated at even decrease low cost charges nonetheless (there are arguments for and in opposition to, however none of it’s talked about and nor are the implications drawn to the Minister’s consideration).

- they notice the excellence that one price might be used for industrial initiatives and one for non-commercial issues, however provide no evaluation or recommendation on both why such a distinction needs to be launched or how, both conceptually or virtually, the 2 can be distinguished (they promise they’d develop future steerage, however this nonetheless seems to not have been performed).

- they by no means draw the Minister’s consideration to the truth that one can consider initiatives at any price one chooses however that it doesn’t change the actual fact that there’s a actual value – in debt and fairness finance – which isn’t 1,000,000 miles away from the Social Alternative Price (SOC) strategy they had been planning to maneuver away from. Tasks that handed a cost-benefit check at a 2% (or 1%) low cost price however failed to take action utilizing an 8 per cent price would, if authorised, merely be being subsidised by taxpayers.

- they by no means drew to the Minister’s consideration that they had been planning to go away the speed of capital cost at 5 per cent, now inconsistent with both strategy to discounting and venture analysis

There’s additionally no engagement with a few of the conceptual points raised by what Treasury was planning. That is from my earlier submit

It’s all very effectively for Treasury to say that each proposal must have numbers introduced with each a 2% and eight% low cost price, but when they can not reply easy questions like these (or alert the Minister to them) then all they’ve performed is launched a pro-more-spending muddled mannequin.

Maybe most breathtaking was the daring declare (supplied with no supporting evaluation in any respect) that “The up to date low cost charges is not going to change the greenback quantity of spending, since particular person spending proposals will proceed to be prioritised inside a price range constraint (fiscal allowances).”

It’s the form of declare that if a primary 12 months analyst had made you may take them apart and clarify one thing about incentives, political economic system, and what was and wasn’t mounted within the system. This paper was written and signed out by a extremely skilled Principal Adviser and a extremely skilled Supervisor, and the coverage had been signed off by the complete Government Management group.

By no means as soon as it’s identified to the Minister that price range allowances (whether or not capital or working) are hardly immoveable stakes within the floor, enduring come hell or excessive water from decade to decade. (Why, this very morning, the working allowance for this 12 months was altered once more). Or that the general impact of what Treasury was planning on doing would imply that extra initiatives (spending proposals) and extra regulatory initiatives would go a cost-benefit check and present a optimistic web current worth. And that whereas, in any explicit 12 months, an working allowance may bind (in order that solely – at the very least in precept – essentially the most extremely ranked initiatives (in NPV phrases) would get authorised, over time if extra initiatives and regulatory proposals confirmed up with optimistic NPVs the stress can be more likely to mount – whether or not from public sector businesses or exterior foyer teams – for extra spending and extra regulation. (In reality, Treasury by no means even identified the working allowance is a web new initiatives determine and better taxes can enable greater spending even inside that self-imposed momentary constraint.) And that even when a Nationwide Social gathering minister may pleasure herself on her authorities’s supposed means to restrain spending, time will go, governments will change, and future governments which can be predisposed to spend extra will maintain workplace. Sharply reducing low cost charges – to miles beneath the precise value of capital – was simply an invite to such governments. It looks like fiscal political economic system 101…..and but not solely is that this problem not touched on within the recommendation to the Minister there is no such thing as a signal of it in any of the opposite paperwork Treasury launched to me. You wouldn’t get the sense in any respect both that the fiscal start line was one through which New Zealand now had one of many largest structural deficits within the superior world, with even a projected return to surplus years away.

Treasury appears to have simply wished decrease low cost charges.

You get this sense on this extract from that brief paper to the Minister

Goodness, we wouldn’t need anybody debating the suitable low cost price would we, so let’s simply render it moot by shifting to a particularly low price (in a rustic with a traditionally excessive – by worldwide requirements – value of capital). Or, we don’t anybody fudging their cost-benefit evaluation – however isn’t Treasury speculated to be a few of gatekeeper and guardian of requirements – so we’ll simply make it straightforward and slash the low cost price vastly. And as for that declare {that a} 5 per cent low cost price – miles beneath any credible estimate of value of capital or personal sector required hurdle price of return – incentivises decisionmakers to give attention to the short-term, there is no such thing as a severe (or unserious) evaluation introduced to the Minister suggesting this was in reality so (that numerous initiatives with compelling instances had been lacking out), nor any try to recommend that capital is in reality pricey, and that when it’s pricey there needs to be a excessive hurdle usually earlier than spending cash that has payoffs solely far into the longer term.

There’s, you must notice, no corresponding paragraph outlining the motivation results and dangers round what Treasury was planning on doing.

There was a time when you possibly can depend on The Treasury for actually good and severe coverage recommendation. If this paper is something to go by, that day is gone. Modifications of this magnitude ought to have been performed solely with the Minister’s express approval and may most likely solely have been performed after severe and open public session. And the Minister was entitled to count on a lot better, and fewer loaded, recommendation than she acquired on this problem, the place what Treasury was planning ran instantly counter to the general route of the federal government fiscal coverage and spending rhetoric. The Minister herself most likely ought to have had higher and extra demanding advisers in her workplace, however actually the prime duty right here for a nasty, muddled and ill-justified change of coverage rests with The Treasury.

(And in case you assume I’m a lone voice in having considerations, right here is column from a former very skilled Treasury official who had appreciable expertise in these and associated points)

A few months in the past now I wrote a submit in regards to the new set of low cost charges authorities businesses are supposed to make use of in endeavor cost-benefit evaluation, whether or not for brand new spending initiatives or for regulatory initiatives. The brand new, radically altered, framework had come into impact from 1 October final 12 months, however with no publicity (besides to the general public sector businesses required to make use of them). The brand new framework, with a lot decrease low cost charges for many core public sector issues, wasn’t precisely hidden nevertheless it wasn’t marketed both.

My earlier submit (most likely greatest learn along with this one) was primarily based largely round a public seminar Treasury did lastly host in February, the advert for which had belatedly alerted me to this substantial change of coverage strategy (and despatched me off to numerous background paperwork on The Treasury web site).

As a fast reminder, low cost charges matter (usually loads), as they convert future prices and advantages again into equal in the present day’s {dollars} (current values). The low cost price used makes an enormous distinction: for a profit in 30 years time discounting at 2 per cent each year reduces the worth by nearly half, whereas transformed at 8 per cent the current worth of that profit is decreased by nearly 90 per cent.

Till final October, initiatives and initiatives had been to be evaluated at a 5 per cent actual low cost price – slightly decrease than the charges traditionally utilized in New Zealand, however not inconsistent with the document low actual rates of interest skilled across the flip of the last decade (recall that the low cost charges didn’t try to mimic a bond price, however took account of the price of each debt and fairness).

The brand new framework, summarised in a single desk, is

and in case there was any ambiguity about the place the main focus now lay, not solely was the non-commercial proposals line listed first however the round itself made it clear that the non-commercial price(s) had been more likely to be the norm for many public service and Crown entity proposals.

Within the earlier submit I outlined a bunch of considerations about this new strategy, each across the substance and what it would imply for future spending (and, for that matter, regulatory) pressures, and round what appeared to have been fairly a rare course of, with no public session in any respect. Treasury officers on the seminar had, nevertheless, assured me that it had all been authorised by the Minister of Finance, which frankly appeared a bit odd given the (then) new authorities’s rhetorical give attention to rigorous analysis of spending proposals and so on.

Anyway, I went dwelling and lodged an Official Data Act request with The Treasury. They dealt with it pretty expeditiously nevertheless it took me some time to get spherical to working my manner by means of the 100+ pages they supplied. This was the discharge they made to me

Treasury OIA re Public Sector Low cost Charges March 2025

and this was their recommendation to the Minister of Finance, already launched however buried very deep in an enormous normal launch on a spread of matters. I’ve saved it right here as a separate doc.

Treasury Report: Updates to Public Sector Low cost Charges 30 July 2024

Not one of the launched materials allayed any of my considerations. In reality, these considerations at the moment are amplified, and added to them is a priority in regards to the actually poor high quality, and loaded nature, of the slim recommendation supplied to the Minister of Finance on what may be actually fairly a technical problem however with a lot wider potential political economic system implications. There was an finish to be achieved – officers had been eager on decrease low cost charges – and by no means thoughts a cautious. balanced, and complete perspective. It was maybe summed up within the remark from one principal adviser who famous “I get a bit misplaced on the technical forwards and backwards on SOC vs SRTP” however “I assist shifting to 2%”.

Considerably amazingly, though all of the paperwork speak about how a change of this type actually ought to have ministerial approval – that is even documented within the minutes of The Treasury’s Government Management Group assembly of 12 March 2024 – ultimately all they did was ask the Minister to notice the change they (officers) had been making. All of the Minister was requested to comply with was course of stuff across the begin date and future critiques. I’m stunned that there appears to have been nobody in her workplace – her non-Treasury advisers, who partly are supposed to guard busy and non-technical ministers from officers with an agenda – who seems to have appreciated the importance of what was happening or thus to have triggered a request for extra and higher evaluation/recommendation. And even, it seems, to have raised questions on what was behind the remark within the Session part of the paper that “To handle dangers of elevating exterior expectations and a danger of extended debate, we’ve not consulted publicly”. Had been there maybe various views then that the Minister ought to have been made conscious of? (The one individuals consulted had been different public sector chief economists – whose businesses will usually be eager on getting venture analysis thresholds lowered – and some handpicked consultants.)

What turned extra obvious within the papers was that this complete venture had obtained going below the earlier authorities (Labour, however with Greens ministers) when the Parliamentary Commissioner for the Surroundings had instructed in 2021 that public low cost charges needs to be reviewed with a view to adopting a mannequin that might low cost future advantages (relative to upfront prices) much less closely. Treasury had undertaken in 2022 to the (then Labour majority) choose committee that they’d do a overview. Issues appeared to get their very own momentum from there, and nothing about both a change in fiscal circumstances – again in 2021/22 even Treasury was eager on spraying public cash round – nor a change in authorities appears to have prompted a pause. Had the brand new Minister of Finance, or her workplace, been extra alert to the implications, maybe they’d have referred to as a halt to the work programme (however on this event I’m reluctant to place a lot blame on the Minister, as she seems to have been so badly suggested by The Treasury).

The one recommendation the Minister of Finance seems to have been supplied with is the brief paper linked to above. It has simply over two pages of substance (the remaining is course of, plus a 4 web page technical appendix – which I’d think about that, for a noting suggestion solely, a busy – and non-technical – minister wouldn’t usually learn).

It’s placing what the Minister isn’t advised:

- there is no such thing as a point out within the paper that the sensible implication of the brand new strategy Treasury was planning to take was that the majority public sector initiatives and proposals can be evaluated main at a 2 per cent actual low cost price slightly than the (customary) 5 per cent price beforehand. They point out that the SOC-based price is being elevated, in step with the rise in bond charges, however by no means that this low cost price will not be used a lot.

- there is no such thing as a try within the paper to the Minister to clarify, or justify, the brand new strategy below which low cost charges for years past 12 months 30 can be evaluated at even decrease low cost charges nonetheless (there are arguments for and in opposition to, however none of it’s talked about and nor are the implications drawn to the Minister’s consideration).

- they notice the excellence that one price might be used for industrial initiatives and one for non-commercial issues, however provide no evaluation or recommendation on both why such a distinction needs to be launched or how, both conceptually or virtually, the 2 can be distinguished (they promise they’d develop future steerage, however this nonetheless seems to not have been performed).

- they by no means draw the Minister’s consideration to the truth that one can consider initiatives at any price one chooses however that it doesn’t change the actual fact that there’s a actual value – in debt and fairness finance – which isn’t 1,000,000 miles away from the Social Alternative Price (SOC) strategy they had been planning to maneuver away from. Tasks that handed a cost-benefit check at a 2% (or 1%) low cost price however failed to take action utilizing an 8 per cent price would, if authorised, merely be being subsidised by taxpayers.

- they by no means drew to the Minister’s consideration that they had been planning to go away the speed of capital cost at 5 per cent, now inconsistent with both strategy to discounting and venture analysis

There’s additionally no engagement with a few of the conceptual points raised by what Treasury was planning. That is from my earlier submit

It’s all very effectively for Treasury to say that each proposal must have numbers introduced with each a 2% and eight% low cost price, but when they can not reply easy questions like these (or alert the Minister to them) then all they’ve performed is launched a pro-more-spending muddled mannequin.

Maybe most breathtaking was the daring declare (supplied with no supporting evaluation in any respect) that “The up to date low cost charges is not going to change the greenback quantity of spending, since particular person spending proposals will proceed to be prioritised inside a price range constraint (fiscal allowances).”

It’s the form of declare that if a primary 12 months analyst had made you may take them apart and clarify one thing about incentives, political economic system, and what was and wasn’t mounted within the system. This paper was written and signed out by a extremely skilled Principal Adviser and a extremely skilled Supervisor, and the coverage had been signed off by the complete Government Management group.

By no means as soon as it’s identified to the Minister that price range allowances (whether or not capital or working) are hardly immoveable stakes within the floor, enduring come hell or excessive water from decade to decade. (Why, this very morning, the working allowance for this 12 months was altered once more). Or that the general impact of what Treasury was planning on doing would imply that extra initiatives (spending proposals) and extra regulatory initiatives would go a cost-benefit check and present a optimistic web current worth. And that whereas, in any explicit 12 months, an working allowance may bind (in order that solely – at the very least in precept – essentially the most extremely ranked initiatives (in NPV phrases) would get authorised, over time if extra initiatives and regulatory proposals confirmed up with optimistic NPVs the stress can be more likely to mount – whether or not from public sector businesses or exterior foyer teams – for extra spending and extra regulation. (In reality, Treasury by no means even identified the working allowance is a web new initiatives determine and better taxes can enable greater spending even inside that self-imposed momentary constraint.) And that even when a Nationwide Social gathering minister may pleasure herself on her authorities’s supposed means to restrain spending, time will go, governments will change, and future governments which can be predisposed to spend extra will maintain workplace. Sharply reducing low cost charges – to miles beneath the precise value of capital – was simply an invite to such governments. It looks like fiscal political economic system 101…..and but not solely is that this problem not touched on within the recommendation to the Minister there is no such thing as a signal of it in any of the opposite paperwork Treasury launched to me. You wouldn’t get the sense in any respect both that the fiscal start line was one through which New Zealand now had one of many largest structural deficits within the superior world, with even a projected return to surplus years away.

Treasury appears to have simply wished decrease low cost charges.

You get this sense on this extract from that brief paper to the Minister

Goodness, we wouldn’t need anybody debating the suitable low cost price would we, so let’s simply render it moot by shifting to a particularly low price (in a rustic with a traditionally excessive – by worldwide requirements – value of capital). Or, we don’t anybody fudging their cost-benefit evaluation – however isn’t Treasury speculated to be a few of gatekeeper and guardian of requirements – so we’ll simply make it straightforward and slash the low cost price vastly. And as for that declare {that a} 5 per cent low cost price – miles beneath any credible estimate of value of capital or personal sector required hurdle price of return – incentivises decisionmakers to give attention to the short-term, there is no such thing as a severe (or unserious) evaluation introduced to the Minister suggesting this was in reality so (that numerous initiatives with compelling instances had been lacking out), nor any try to recommend that capital is in reality pricey, and that when it’s pricey there needs to be a excessive hurdle usually earlier than spending cash that has payoffs solely far into the longer term.

There’s, you must notice, no corresponding paragraph outlining the motivation results and dangers round what Treasury was planning on doing.

There was a time when you possibly can depend on The Treasury for actually good and severe coverage recommendation. If this paper is something to go by, that day is gone. Modifications of this magnitude ought to have been performed solely with the Minister’s express approval and may most likely solely have been performed after severe and open public session. And the Minister was entitled to count on a lot better, and fewer loaded, recommendation than she acquired on this problem, the place what Treasury was planning ran instantly counter to the general route of the federal government fiscal coverage and spending rhetoric. The Minister herself most likely ought to have had higher and extra demanding advisers in her workplace, however actually the prime duty right here for a nasty, muddled and ill-justified change of coverage rests with The Treasury.

(And in case you assume I’m a lone voice in having considerations, right here is column from a former very skilled Treasury official who had appreciable expertise in these and associated points)

A few months in the past now I wrote a submit in regards to the new set of low cost charges authorities businesses are supposed to make use of in endeavor cost-benefit evaluation, whether or not for brand new spending initiatives or for regulatory initiatives. The brand new, radically altered, framework had come into impact from 1 October final 12 months, however with no publicity (besides to the general public sector businesses required to make use of them). The brand new framework, with a lot decrease low cost charges for many core public sector issues, wasn’t precisely hidden nevertheless it wasn’t marketed both.

My earlier submit (most likely greatest learn along with this one) was primarily based largely round a public seminar Treasury did lastly host in February, the advert for which had belatedly alerted me to this substantial change of coverage strategy (and despatched me off to numerous background paperwork on The Treasury web site).

As a fast reminder, low cost charges matter (usually loads), as they convert future prices and advantages again into equal in the present day’s {dollars} (current values). The low cost price used makes an enormous distinction: for a profit in 30 years time discounting at 2 per cent each year reduces the worth by nearly half, whereas transformed at 8 per cent the current worth of that profit is decreased by nearly 90 per cent.

Till final October, initiatives and initiatives had been to be evaluated at a 5 per cent actual low cost price – slightly decrease than the charges traditionally utilized in New Zealand, however not inconsistent with the document low actual rates of interest skilled across the flip of the last decade (recall that the low cost charges didn’t try to mimic a bond price, however took account of the price of each debt and fairness).

The brand new framework, summarised in a single desk, is

and in case there was any ambiguity about the place the main focus now lay, not solely was the non-commercial proposals line listed first however the round itself made it clear that the non-commercial price(s) had been more likely to be the norm for many public service and Crown entity proposals.

Within the earlier submit I outlined a bunch of considerations about this new strategy, each across the substance and what it would imply for future spending (and, for that matter, regulatory) pressures, and round what appeared to have been fairly a rare course of, with no public session in any respect. Treasury officers on the seminar had, nevertheless, assured me that it had all been authorised by the Minister of Finance, which frankly appeared a bit odd given the (then) new authorities’s rhetorical give attention to rigorous analysis of spending proposals and so on.

Anyway, I went dwelling and lodged an Official Data Act request with The Treasury. They dealt with it pretty expeditiously nevertheless it took me some time to get spherical to working my manner by means of the 100+ pages they supplied. This was the discharge they made to me

Treasury OIA re Public Sector Low cost Charges March 2025

and this was their recommendation to the Minister of Finance, already launched however buried very deep in an enormous normal launch on a spread of matters. I’ve saved it right here as a separate doc.

Treasury Report: Updates to Public Sector Low cost Charges 30 July 2024

Not one of the launched materials allayed any of my considerations. In reality, these considerations at the moment are amplified, and added to them is a priority in regards to the actually poor high quality, and loaded nature, of the slim recommendation supplied to the Minister of Finance on what may be actually fairly a technical problem however with a lot wider potential political economic system implications. There was an finish to be achieved – officers had been eager on decrease low cost charges – and by no means thoughts a cautious. balanced, and complete perspective. It was maybe summed up within the remark from one principal adviser who famous “I get a bit misplaced on the technical forwards and backwards on SOC vs SRTP” however “I assist shifting to 2%”.

Considerably amazingly, though all of the paperwork speak about how a change of this type actually ought to have ministerial approval – that is even documented within the minutes of The Treasury’s Government Management Group assembly of 12 March 2024 – ultimately all they did was ask the Minister to notice the change they (officers) had been making. All of the Minister was requested to comply with was course of stuff across the begin date and future critiques. I’m stunned that there appears to have been nobody in her workplace – her non-Treasury advisers, who partly are supposed to guard busy and non-technical ministers from officers with an agenda – who seems to have appreciated the importance of what was happening or thus to have triggered a request for extra and higher evaluation/recommendation. And even, it seems, to have raised questions on what was behind the remark within the Session part of the paper that “To handle dangers of elevating exterior expectations and a danger of extended debate, we’ve not consulted publicly”. Had been there maybe various views then that the Minister ought to have been made conscious of? (The one individuals consulted had been different public sector chief economists – whose businesses will usually be eager on getting venture analysis thresholds lowered – and some handpicked consultants.)

What turned extra obvious within the papers was that this complete venture had obtained going below the earlier authorities (Labour, however with Greens ministers) when the Parliamentary Commissioner for the Surroundings had instructed in 2021 that public low cost charges needs to be reviewed with a view to adopting a mannequin that might low cost future advantages (relative to upfront prices) much less closely. Treasury had undertaken in 2022 to the (then Labour majority) choose committee that they’d do a overview. Issues appeared to get their very own momentum from there, and nothing about both a change in fiscal circumstances – again in 2021/22 even Treasury was eager on spraying public cash round – nor a change in authorities appears to have prompted a pause. Had the brand new Minister of Finance, or her workplace, been extra alert to the implications, maybe they’d have referred to as a halt to the work programme (however on this event I’m reluctant to place a lot blame on the Minister, as she seems to have been so badly suggested by The Treasury).

The one recommendation the Minister of Finance seems to have been supplied with is the brief paper linked to above. It has simply over two pages of substance (the remaining is course of, plus a 4 web page technical appendix – which I’d think about that, for a noting suggestion solely, a busy – and non-technical – minister wouldn’t usually learn).

It’s placing what the Minister isn’t advised:

- there is no such thing as a point out within the paper that the sensible implication of the brand new strategy Treasury was planning to take was that the majority public sector initiatives and proposals can be evaluated main at a 2 per cent actual low cost price slightly than the (customary) 5 per cent price beforehand. They point out that the SOC-based price is being elevated, in step with the rise in bond charges, however by no means that this low cost price will not be used a lot.

- there is no such thing as a try within the paper to the Minister to clarify, or justify, the brand new strategy below which low cost charges for years past 12 months 30 can be evaluated at even decrease low cost charges nonetheless (there are arguments for and in opposition to, however none of it’s talked about and nor are the implications drawn to the Minister’s consideration).

- they notice the excellence that one price might be used for industrial initiatives and one for non-commercial issues, however provide no evaluation or recommendation on both why such a distinction needs to be launched or how, both conceptually or virtually, the 2 can be distinguished (they promise they’d develop future steerage, however this nonetheless seems to not have been performed).

- they by no means draw the Minister’s consideration to the truth that one can consider initiatives at any price one chooses however that it doesn’t change the actual fact that there’s a actual value – in debt and fairness finance – which isn’t 1,000,000 miles away from the Social Alternative Price (SOC) strategy they had been planning to maneuver away from. Tasks that handed a cost-benefit check at a 2% (or 1%) low cost price however failed to take action utilizing an 8 per cent price would, if authorised, merely be being subsidised by taxpayers.

- they by no means drew to the Minister’s consideration that they had been planning to go away the speed of capital cost at 5 per cent, now inconsistent with both strategy to discounting and venture analysis

There’s additionally no engagement with a few of the conceptual points raised by what Treasury was planning. That is from my earlier submit

It’s all very effectively for Treasury to say that each proposal must have numbers introduced with each a 2% and eight% low cost price, but when they can not reply easy questions like these (or alert the Minister to them) then all they’ve performed is launched a pro-more-spending muddled mannequin.

Maybe most breathtaking was the daring declare (supplied with no supporting evaluation in any respect) that “The up to date low cost charges is not going to change the greenback quantity of spending, since particular person spending proposals will proceed to be prioritised inside a price range constraint (fiscal allowances).”

It’s the form of declare that if a primary 12 months analyst had made you may take them apart and clarify one thing about incentives, political economic system, and what was and wasn’t mounted within the system. This paper was written and signed out by a extremely skilled Principal Adviser and a extremely skilled Supervisor, and the coverage had been signed off by the complete Government Management group.

By no means as soon as it’s identified to the Minister that price range allowances (whether or not capital or working) are hardly immoveable stakes within the floor, enduring come hell or excessive water from decade to decade. (Why, this very morning, the working allowance for this 12 months was altered once more). Or that the general impact of what Treasury was planning on doing would imply that extra initiatives (spending proposals) and extra regulatory initiatives would go a cost-benefit check and present a optimistic web current worth. And that whereas, in any explicit 12 months, an working allowance may bind (in order that solely – at the very least in precept – essentially the most extremely ranked initiatives (in NPV phrases) would get authorised, over time if extra initiatives and regulatory proposals confirmed up with optimistic NPVs the stress can be more likely to mount – whether or not from public sector businesses or exterior foyer teams – for extra spending and extra regulation. (In reality, Treasury by no means even identified the working allowance is a web new initiatives determine and better taxes can enable greater spending even inside that self-imposed momentary constraint.) And that even when a Nationwide Social gathering minister may pleasure herself on her authorities’s supposed means to restrain spending, time will go, governments will change, and future governments which can be predisposed to spend extra will maintain workplace. Sharply reducing low cost charges – to miles beneath the precise value of capital – was simply an invite to such governments. It looks like fiscal political economic system 101…..and but not solely is that this problem not touched on within the recommendation to the Minister there is no such thing as a signal of it in any of the opposite paperwork Treasury launched to me. You wouldn’t get the sense in any respect both that the fiscal start line was one through which New Zealand now had one of many largest structural deficits within the superior world, with even a projected return to surplus years away.

Treasury appears to have simply wished decrease low cost charges.

You get this sense on this extract from that brief paper to the Minister

Goodness, we wouldn’t need anybody debating the suitable low cost price would we, so let’s simply render it moot by shifting to a particularly low price (in a rustic with a traditionally excessive – by worldwide requirements – value of capital). Or, we don’t anybody fudging their cost-benefit evaluation – however isn’t Treasury speculated to be a few of gatekeeper and guardian of requirements – so we’ll simply make it straightforward and slash the low cost price vastly. And as for that declare {that a} 5 per cent low cost price – miles beneath any credible estimate of value of capital or personal sector required hurdle price of return – incentivises decisionmakers to give attention to the short-term, there is no such thing as a severe (or unserious) evaluation introduced to the Minister suggesting this was in reality so (that numerous initiatives with compelling instances had been lacking out), nor any try to recommend that capital is in reality pricey, and that when it’s pricey there needs to be a excessive hurdle usually earlier than spending cash that has payoffs solely far into the longer term.

There’s, you must notice, no corresponding paragraph outlining the motivation results and dangers round what Treasury was planning on doing.

There was a time when you possibly can depend on The Treasury for actually good and severe coverage recommendation. If this paper is something to go by, that day is gone. Modifications of this magnitude ought to have been performed solely with the Minister’s express approval and may most likely solely have been performed after severe and open public session. And the Minister was entitled to count on a lot better, and fewer loaded, recommendation than she acquired on this problem, the place what Treasury was planning ran instantly counter to the general route of the federal government fiscal coverage and spending rhetoric. The Minister herself most likely ought to have had higher and extra demanding advisers in her workplace, however actually the prime duty right here for a nasty, muddled and ill-justified change of coverage rests with The Treasury.

(And in case you assume I’m a lone voice in having considerations, right here is column from a former very skilled Treasury official who had appreciable expertise in these and associated points)

A few months in the past now I wrote a submit in regards to the new set of low cost charges authorities businesses are supposed to make use of in endeavor cost-benefit evaluation, whether or not for brand new spending initiatives or for regulatory initiatives. The brand new, radically altered, framework had come into impact from 1 October final 12 months, however with no publicity (besides to the general public sector businesses required to make use of them). The brand new framework, with a lot decrease low cost charges for many core public sector issues, wasn’t precisely hidden nevertheless it wasn’t marketed both.

My earlier submit (most likely greatest learn along with this one) was primarily based largely round a public seminar Treasury did lastly host in February, the advert for which had belatedly alerted me to this substantial change of coverage strategy (and despatched me off to numerous background paperwork on The Treasury web site).

As a fast reminder, low cost charges matter (usually loads), as they convert future prices and advantages again into equal in the present day’s {dollars} (current values). The low cost price used makes an enormous distinction: for a profit in 30 years time discounting at 2 per cent each year reduces the worth by nearly half, whereas transformed at 8 per cent the current worth of that profit is decreased by nearly 90 per cent.

Till final October, initiatives and initiatives had been to be evaluated at a 5 per cent actual low cost price – slightly decrease than the charges traditionally utilized in New Zealand, however not inconsistent with the document low actual rates of interest skilled across the flip of the last decade (recall that the low cost charges didn’t try to mimic a bond price, however took account of the price of each debt and fairness).

The brand new framework, summarised in a single desk, is

and in case there was any ambiguity about the place the main focus now lay, not solely was the non-commercial proposals line listed first however the round itself made it clear that the non-commercial price(s) had been more likely to be the norm for many public service and Crown entity proposals.

Within the earlier submit I outlined a bunch of considerations about this new strategy, each across the substance and what it would imply for future spending (and, for that matter, regulatory) pressures, and round what appeared to have been fairly a rare course of, with no public session in any respect. Treasury officers on the seminar had, nevertheless, assured me that it had all been authorised by the Minister of Finance, which frankly appeared a bit odd given the (then) new authorities’s rhetorical give attention to rigorous analysis of spending proposals and so on.

Anyway, I went dwelling and lodged an Official Data Act request with The Treasury. They dealt with it pretty expeditiously nevertheless it took me some time to get spherical to working my manner by means of the 100+ pages they supplied. This was the discharge they made to me

Treasury OIA re Public Sector Low cost Charges March 2025

and this was their recommendation to the Minister of Finance, already launched however buried very deep in an enormous normal launch on a spread of matters. I’ve saved it right here as a separate doc.

Treasury Report: Updates to Public Sector Low cost Charges 30 July 2024

Not one of the launched materials allayed any of my considerations. In reality, these considerations at the moment are amplified, and added to them is a priority in regards to the actually poor high quality, and loaded nature, of the slim recommendation supplied to the Minister of Finance on what may be actually fairly a technical problem however with a lot wider potential political economic system implications. There was an finish to be achieved – officers had been eager on decrease low cost charges – and by no means thoughts a cautious. balanced, and complete perspective. It was maybe summed up within the remark from one principal adviser who famous “I get a bit misplaced on the technical forwards and backwards on SOC vs SRTP” however “I assist shifting to 2%”.

Considerably amazingly, though all of the paperwork speak about how a change of this type actually ought to have ministerial approval – that is even documented within the minutes of The Treasury’s Government Management Group assembly of 12 March 2024 – ultimately all they did was ask the Minister to notice the change they (officers) had been making. All of the Minister was requested to comply with was course of stuff across the begin date and future critiques. I’m stunned that there appears to have been nobody in her workplace – her non-Treasury advisers, who partly are supposed to guard busy and non-technical ministers from officers with an agenda – who seems to have appreciated the importance of what was happening or thus to have triggered a request for extra and higher evaluation/recommendation. And even, it seems, to have raised questions on what was behind the remark within the Session part of the paper that “To handle dangers of elevating exterior expectations and a danger of extended debate, we’ve not consulted publicly”. Had been there maybe various views then that the Minister ought to have been made conscious of? (The one individuals consulted had been different public sector chief economists – whose businesses will usually be eager on getting venture analysis thresholds lowered – and some handpicked consultants.)

What turned extra obvious within the papers was that this complete venture had obtained going below the earlier authorities (Labour, however with Greens ministers) when the Parliamentary Commissioner for the Surroundings had instructed in 2021 that public low cost charges needs to be reviewed with a view to adopting a mannequin that might low cost future advantages (relative to upfront prices) much less closely. Treasury had undertaken in 2022 to the (then Labour majority) choose committee that they’d do a overview. Issues appeared to get their very own momentum from there, and nothing about both a change in fiscal circumstances – again in 2021/22 even Treasury was eager on spraying public cash round – nor a change in authorities appears to have prompted a pause. Had the brand new Minister of Finance, or her workplace, been extra alert to the implications, maybe they’d have referred to as a halt to the work programme (however on this event I’m reluctant to place a lot blame on the Minister, as she seems to have been so badly suggested by The Treasury).

The one recommendation the Minister of Finance seems to have been supplied with is the brief paper linked to above. It has simply over two pages of substance (the remaining is course of, plus a 4 web page technical appendix – which I’d think about that, for a noting suggestion solely, a busy – and non-technical – minister wouldn’t usually learn).

It’s placing what the Minister isn’t advised:

- there is no such thing as a point out within the paper that the sensible implication of the brand new strategy Treasury was planning to take was that the majority public sector initiatives and proposals can be evaluated main at a 2 per cent actual low cost price slightly than the (customary) 5 per cent price beforehand. They point out that the SOC-based price is being elevated, in step with the rise in bond charges, however by no means that this low cost price will not be used a lot.

- there is no such thing as a try within the paper to the Minister to clarify, or justify, the brand new strategy below which low cost charges for years past 12 months 30 can be evaluated at even decrease low cost charges nonetheless (there are arguments for and in opposition to, however none of it’s talked about and nor are the implications drawn to the Minister’s consideration).

- they notice the excellence that one price might be used for industrial initiatives and one for non-commercial issues, however provide no evaluation or recommendation on both why such a distinction needs to be launched or how, both conceptually or virtually, the 2 can be distinguished (they promise they’d develop future steerage, however this nonetheless seems to not have been performed).

- they by no means draw the Minister’s consideration to the truth that one can consider initiatives at any price one chooses however that it doesn’t change the actual fact that there’s a actual value – in debt and fairness finance – which isn’t 1,000,000 miles away from the Social Alternative Price (SOC) strategy they had been planning to maneuver away from. Tasks that handed a cost-benefit check at a 2% (or 1%) low cost price however failed to take action utilizing an 8 per cent price would, if authorised, merely be being subsidised by taxpayers.

- they by no means drew to the Minister’s consideration that they had been planning to go away the speed of capital cost at 5 per cent, now inconsistent with both strategy to discounting and venture analysis

There’s additionally no engagement with a few of the conceptual points raised by what Treasury was planning. That is from my earlier submit

It’s all very effectively for Treasury to say that each proposal must have numbers introduced with each a 2% and eight% low cost price, but when they can not reply easy questions like these (or alert the Minister to them) then all they’ve performed is launched a pro-more-spending muddled mannequin.

Maybe most breathtaking was the daring declare (supplied with no supporting evaluation in any respect) that “The up to date low cost charges is not going to change the greenback quantity of spending, since particular person spending proposals will proceed to be prioritised inside a price range constraint (fiscal allowances).”

It’s the form of declare that if a primary 12 months analyst had made you may take them apart and clarify one thing about incentives, political economic system, and what was and wasn’t mounted within the system. This paper was written and signed out by a extremely skilled Principal Adviser and a extremely skilled Supervisor, and the coverage had been signed off by the complete Government Management group.

By no means as soon as it’s identified to the Minister that price range allowances (whether or not capital or working) are hardly immoveable stakes within the floor, enduring come hell or excessive water from decade to decade. (Why, this very morning, the working allowance for this 12 months was altered once more). Or that the general impact of what Treasury was planning on doing would imply that extra initiatives (spending proposals) and extra regulatory initiatives would go a cost-benefit check and present a optimistic web current worth. And that whereas, in any explicit 12 months, an working allowance may bind (in order that solely – at the very least in precept – essentially the most extremely ranked initiatives (in NPV phrases) would get authorised, over time if extra initiatives and regulatory proposals confirmed up with optimistic NPVs the stress can be more likely to mount – whether or not from public sector businesses or exterior foyer teams – for extra spending and extra regulation. (In reality, Treasury by no means even identified the working allowance is a web new initiatives determine and better taxes can enable greater spending even inside that self-imposed momentary constraint.) And that even when a Nationwide Social gathering minister may pleasure herself on her authorities’s supposed means to restrain spending, time will go, governments will change, and future governments which can be predisposed to spend extra will maintain workplace. Sharply reducing low cost charges – to miles beneath the precise value of capital – was simply an invite to such governments. It looks like fiscal political economic system 101…..and but not solely is that this problem not touched on within the recommendation to the Minister there is no such thing as a signal of it in any of the opposite paperwork Treasury launched to me. You wouldn’t get the sense in any respect both that the fiscal start line was one through which New Zealand now had one of many largest structural deficits within the superior world, with even a projected return to surplus years away.

Treasury appears to have simply wished decrease low cost charges.

You get this sense on this extract from that brief paper to the Minister

Goodness, we wouldn’t need anybody debating the suitable low cost price would we, so let’s simply render it moot by shifting to a particularly low price (in a rustic with a traditionally excessive – by worldwide requirements – value of capital). Or, we don’t anybody fudging their cost-benefit evaluation – however isn’t Treasury speculated to be a few of gatekeeper and guardian of requirements – so we’ll simply make it straightforward and slash the low cost price vastly. And as for that declare {that a} 5 per cent low cost price – miles beneath any credible estimate of value of capital or personal sector required hurdle price of return – incentivises decisionmakers to give attention to the short-term, there is no such thing as a severe (or unserious) evaluation introduced to the Minister suggesting this was in reality so (that numerous initiatives with compelling instances had been lacking out), nor any try to recommend that capital is in reality pricey, and that when it’s pricey there needs to be a excessive hurdle usually earlier than spending cash that has payoffs solely far into the longer term.

There’s, you must notice, no corresponding paragraph outlining the motivation results and dangers round what Treasury was planning on doing.

There was a time when you possibly can depend on The Treasury for actually good and severe coverage recommendation. If this paper is something to go by, that day is gone. Modifications of this magnitude ought to have been performed solely with the Minister’s express approval and may most likely solely have been performed after severe and open public session. And the Minister was entitled to count on a lot better, and fewer loaded, recommendation than she acquired on this problem, the place what Treasury was planning ran instantly counter to the general route of the federal government fiscal coverage and spending rhetoric. The Minister herself most likely ought to have had higher and extra demanding advisers in her workplace, however actually the prime duty right here for a nasty, muddled and ill-justified change of coverage rests with The Treasury.

(And in case you assume I’m a lone voice in having considerations, right here is column from a former very skilled Treasury official who had appreciable expertise in these and associated points)

{kind=link}